Landlord Products / Services

Landlord Products / Services

Nope! Cash House Buyer companies certainly ain’t for everyone, especially if you’re looking to squeeze every last penny out of your property based on its current market value and there’s no wiggle room! If that’s you, you may as well turn around and head for the door.

However, if you want a quick, guaranteed sale (in as little as seven days in some cases), choosing a reputable cash house buyer could be the answer to your prayers. They can save you a bunch of of time and stress and, contrary to popular belief, could even save you thousands of pounds. You avoid the uncertainty of failed sales, broken chains, and long waiting periods in slow markets. In a cold or declining property market, this delay can actually work against you, as property values may continue to fall while your home remains unsold.

Using a cash house buying company was once seen as a last resort for “desperate sellers”, but that really isn’t true – many homeowners use them for convenience, speed, and certainty when selling a property.

But the industry has a huge reputation crisis on its hands – shunned by many for being snake-oil charlatans – and, in all fairness, that perception is largely justified. Not all cash buying companies operate fairly – many offer misleading offers, hidden fees, or use aggressive tactics that can leave sellers worse off than expected. There are definitely dark forces in operation.

However, by choosing a reputable company that is transparent about how it works and what it will actually pay, you can still benefit from all the advantages of using a cash buyer.

- Cash offer within 48 hours — with no obligation

- Complete your sale in as little as 7 days

- No fees to pay – all legal and selling costs covered

- Any property considered, regardless of condition

So, should you use a cash house buying company?

This guide compares the best cash house buyer companies in the UK and explains everything you need to know to help you decide whether it’s the right choice for you – including common pitfalls and how to avoid them.

Page contents

- What Are Quick House Sale Companies?

- Best Quick House Sale Companies in the UK

- Pros and Cons of Cash House Buyers

- What to Consider Before Using a Cash House Buyer

- Cash House Buyer Scams and Warning Signs

- Questions to Ask Cash House Buying Companies

- Cash House Buyers vs Estate Agents

- Alternatives to Cash House Buying Companies

What Are Quick House Sale Companies?

Quick house sale companies (also known as ‘We buy any house‘ companies and “Cash House Buyers”) purchase properties directly for cash – typically in any condition. Even your one, probably.

They are commonly used by homeowners who need to sell quickly or who want to avoid the time, cost, and uncertainty involved in traditional estate agency sales, particularly where repairs or renovations would otherwise be required.

They are commonly used by homeowners who need to sell quickly or who want to avoid the time, cost, and uncertainty involved in traditional estate agency sales, particularly where repairs or renovations would otherwise be required.

- Divorce/ separation

- Financial difficulty (e.g. prevent house from being repossessed)

- Selling property in probate

- Inherited a property

- Relocating / emigrating

- Problematic property (e.g. subsidence, Japanese Knotweed, Property with loft foam insulation etc)

Cash house buying companies generally operate in one of two ways:

- Broker model: The company does not purchase the property directly but instead sources a cash buyer in the background and takes a fee for facilitating the sale.

- Direct purchase model: The company buys the property directly from the seller using its own funds. This is typically the fastest route to completion.

In both cases, sellers should expect to receive below full market value – typically around 10%-25% less – in exchange for speed, convenience, and certainty of sale. This is a standard part of the cash buying model rather than a hidden drawback.

Be wary of any property cash buyer that offers 100% of the market value! A genuine property cash buying company will never pay full market value!

Best Quick House Sale Companies in the UK

While I have not personally used any of the companies listed below (and therefore cannot recommend them based on direct experience), I have reviewed a wide range of quick house sale services and shortlisted those that appear to be the most reputable and established. I have also spoken with industry experts to help verify my assessment.

I explain how these companies were selected below the table.

I have summarised the key selling features of each service for comparison purposes, but I strongly recommend carrying out your own due diligence before making any decisions.

| Service | Rating | Features | Offers (up to) | |

|---|---|---|---|---|

| My Homebuyers | Rating TrustPilot Reviews | Features

| Offers (up to) 80-85%of Market Value | Get cash offer |

| Home House Buyers | Rating Reviews.co.uk | Features

| Offers (up to) 80-85%of Market Value | Get cash offer |

| House Buy Fast | Rating feefo Reviews | Features

| Offers (up to) 85%of Market Value | Get cash offer |

Property Solvers | Rating TrustPilot Reviews | Features

| Offers (up to) 75%of Market Value | Get cash offer |

Please note, I try my best to keep the information of each service up-to-date, but you should read the T&C's from their website for the most up-to-date and accurate information.

If you have any experience with any of the above companies, or if you’re in the midst of weighing up your options, I’d love to hear your feedback (leave a comment below!).

How did the companies listed make my shortlist?

As mentioned, I have not personally used any of the companies listed, and therefore cannot recommend them based on direct experience. However, I reviewed a wide range of quick house sale services, spoken to industry experts for their insight, and applied a consistent set of criteria to create a shortlist of the most reputable and established providers.

This methodology was designed to provide a balanced and objective comparison based on publicly available information and industry standards.

The companies included were assessed against the following criteria:

- Genuine cash buyers: Companies must purchase properties directly rather than acting solely as intermediaries or brokers. Direct buyers reduce the risk of chain failure and typically offer faster completion times.

- Professional website and user experience: Companies were expected to have a clear, functional, and professional online presence that reflects legitimacy and accessibility.

- Strong independent reviews: Positive ratings across established third-party platforms such as Trustpilot, Feefo, and Reviews.co.uk were considered.

- Membership of redress schemes: Preference was given to companies registered with bodies such as the National Association of Property Buyers (NAPB) and The Property Ombudsman (TPOS), which provide independent dispute resolution.

- Realistic cash offers: Typical offers within the range of approximately 75%–85% of market value were considered consistent with industry norms.

- Transparency of contact details: Companies were expected to provide clear business information, including verifiable contact details and, where applicable, physical office locations.

- Company registration: Active registration with Companies House was used as a baseline indicator of legitimacy.

- Established trading history: Preference was given to companies with a proven track record and established presence in the market.

Now, if there’s a company you’re researching (or representing) that isn’t on my list, before you get all uppity, I want to clarify that while this shortlist has been carefully compiled, it is not exhaustive. There may be reputable companies that are not included, and their absence does not imply a negative judgement (although it quite possibly could).

The aim of this guide is to highlight a small number of established and credible options, rather than provide an overly long list. I generally struggle with long lists of anything, because I don’t find them particularly helpful with decision making, which is why I’ve intentionally kept the list tiny and effective.

Pros and Cons of Cash House Buyers

Pros

- Fast Sale Completion: Achieve a quick sale – these companies usually have the cash available to purchase a property outright, meaning the transaction can be completed in as little as a few days.

- Reduced Hassle: A far simpler process than traditional methods, particularly because all legal work and property searches are handled for you.

- Access to Cash Quickly: A fast way of liquidating an asset in order to access funds when you need them.

- Financial Relief: Can help avoid repossession, clear debts, and generally resolve urgent financial difficulties.

- Alternative to Traditional Selling: A suitable option for anyone who has struggled to sell their property through the open market.

- Useful for Difficult Properties: An effective solution for selling “hard-to-sell” properties, such as those needing significant repair or in low-demand areas. Case in point, here’s a Tweet I randomly bumped into on my timeline, by someone that goes by the alias @landlord_secret:

Cons

- Lower Sale Price Than Market Value: The main trade-off of using a quick house sale service is that you will typically receive less than the open market value (usually around 75%–90%). This is expected, as cash buyers offer speed and certainty in exchange for a discounted price.

- Unregulated Industry: The cash house buying sector in the UK is largely unregulated, making it important to choose a reputable and trustworthy company.

- Unclear Fee Structures: Some companies use complex or unclear fee arrangements, which can result in sellers receiving less than initially expected.

- Risk of Misleading Valuations: Some companies may provide inflated or misleading initial valuations in order to attract sellers, before reducing the offer later in the process.

Needless to say, most of the cons can be avoided with due diligence and by using a reputable company.

What to Consider Before Using a Cash House Buyer

- Consider whether it’s the right option for you: Think carefully about whether a quick house sale company suits your circumstances. It’s important to understand both the advantages and disadvantages, and to compare all available options before making a decision.

- Check your own property valuation: Don’t rely solely on the valuation provided by a quick sale company. Carry out your own independent valuation as well. Here is a guide on how you can value your property.

Be cautious of overly low valuations. There have been reported cases of sellers losing significant value when accepting undervalued offers from quick sale companies.

It is also important to understand how valuations are carried out. Typically, you will receive an initial estimate by phone, followed by a property inspection and a revised offer. You are under no obligation to accept any offer, but always confirm the process before agreeing to an in-person valuation.

- Negotiate where possible: Don’t be afraid to negotiate. Some flexibility may exist depending on the company and the condition of your property.

- Understand “free service” claims: Many quick house sale companies advertise “no fees” or “free legal services” While there are no direct upfront costs to you, these costs are typically reflected in the offer price, which is usually below market value. This is standard practice, but it’s important to be aware of it when comparing offers.

- Check regulation and protections: The cash house buying industry is not fully regulated, meaning consumer protection can vary. To reduce risk, consider using companies that are members of the National Association of Property Buyers (NAPB), as members are required to register with The Property Ombudsman (TPOS).

Independent reporting has highlighted concerns within the industry, including investigations into unfair practices affecting vulnerable sellers. This makes choosing a reputable company especially important.

Only use a cash house buyer that is a member of the National Association of Property Buyers (NAPB) and registered with The Property Ombudsman (TPOS). - Understand the type of service offered: Cash house buyers generally operate in two ways:

- Direct buyer: The company purchases your property directly, typically at a lower price (around 75%-90% of market value), but with a faster completion time (often 7-14 days).

- Broker/service provider: The company finds a third-party buyer, which may result in a higher offer (around 85%-95% of market value), but with a longer timeframe (often 4-8 weeks). These arrangements may also involve exclusivity agreements, similar to estate agents.

- Read all contracts carefully: Ensure you fully understand all terms and conditions before agreeing to anything. Pay close attention to fees, deductions, and timelines. Always rely on written agreements rather than verbal assurances.

- Use an independent solicitor: While many companies recommend their own legal partners, you are not required to use them. It is generally advisable to instruct your own independent solicitor.

If you need one, you can find regulated legal professionals here:

- England and Wales: Law Society website

- Scotland: Law Society of Scotland website

- Northern Ireland: Law Society of Northern Ireland website

- Ask detailed questions: Always ask questions before committing. For example, ask how quickly they can complete the sale, when funds will be transferred, and how many similar transactions they have completed recently. A full list of recommended questions is included later in this guide.

Cash House Buyer Scams and Warning Signs

While there are many reputable cash house buying companies in the UK, the industry is not fully regulated, which means unscrupulous operators do exist. It is important to know what to look out for to avoid potential issues.

Below are some potential red flags to be aware of:

- No membership with industry bodies: If a company is not a registered member of the National Association of Property Buyers (NAPB) or The Property Ombudsman (TPOS), verify their status independently before proceeding.

- Pressure to sign contracts or restrictive agreements: Be cautious of “lock-in” contracts, option agreements, or RX1 restrictions. These can limit your ability to withdraw or explore other offers. In most genuine direct cash purchases, you should not be asked to sign binding agreements early in the process.

- False claims of regulation: Be wary of companies claiming to be “government regulated” or officially approved, as the cash buying industry itself is not directly regulated in the UK.

- Upfront fees or payments: Reputable cash buyers do not charge sellers upfront fees. Any request for payment before completion should be treated as a signal to run.

- Unrealistic offers before valuation: Be cautious if a company provides a formal offer without carrying out a proper property assessment. Inflated initial offers are sometimes used to attract sellers before being reduced later in the process.

- Cancellation or withdrawal fees: Carefully review contracts for any hidden exit fees or penalties for withdrawing from the sale.

- Unrealistically high valuations: Be cautious of companies promising close to full market value (95%-100%), as this is often not commercially realistic in a genuine cash purchase model. If they accurately valued the property at market value and offered that much, they wouldn’t be in business.

- Lack of company transparency: A legitimate company should clearly display its company registration number and business details on its website.

- Acting as a broker without disclosure: Some firms advertise as direct cash buyers but actually act as intermediaries. Always ask whether they are purchasing directly and request proof of funds if needed. Any reputable cash buyer will be happy to prove that they are genuine. If they seem shaky about it, it’s a red flag.

Questions to Ask Cash House Buying Companies

- Which redness schemes are you members of?

Many companies (not just quick house sale companies) advertise they are members of various redness schemes when they actually aren’t! You should be able to verify membership on each respective scheme’s website.

- Do I have to sign any option/purchase agreement with you (basically, find out if you’re tied into any contracts)?

- Are you direct buyers with the finance in place or brokering a deal with a 3rd party cash buyer?

- How will you value my property?

- How long until completion?

- How long after completion will I receive the money?

- Is the valuation 100% free and without any obligations?

- The following questions will typically only be relevant if the company requires the seller to sign a purchase agreement (as mentioned, I would avoid cash buying companies that require it), but still worth asking them even if not:

- What fees will I be obligated to pay, including any charges if the sale doesn’t complete?

- Can I cancel our agreement without incurring any fees/penalties?

- Will I be restricted to using your services (similar to a ‘sole agency’ agreement)?

- Can you at any point change your offer, and if so, on what grounds? If you change your offer can I cancel our agreement without incurring any fees/penalties?

- Will you put a ‘restriction’ against the title of my property with HM Land Registry? (if “yes”, then they will be able to register a charge on your property!)

Important: ask these questions via email so you have written proof of their answers!

Cash House Buyers vs Estate Agents

Ah, some would say the ultimate match-up: Douche-bag Vs Douche-bag

Of course, I’m not one of those people. I’m not a savage.

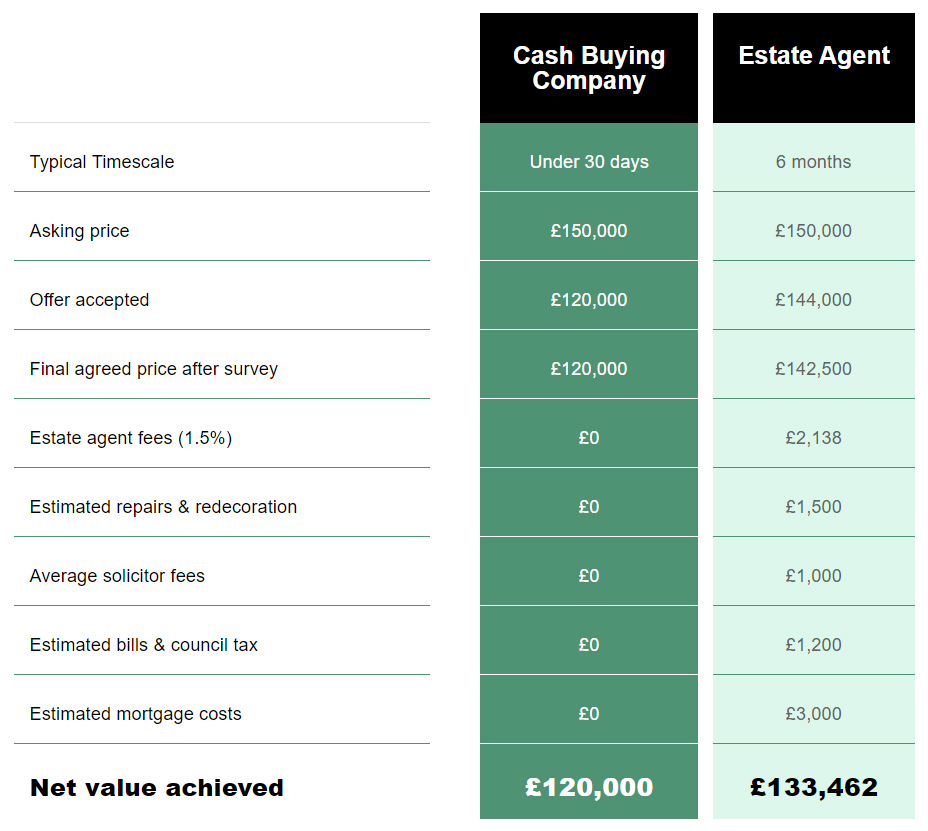

The majority of cash buying companies will occupy their homepage with a nifty little comparison table that highlights their service Vs Estate Agent, which demonstrates a predictably biased overview of why we may want to consider their service over our beloved local high-street estate agency. It goes something like this:

They sure do paint a pretty little picture, don’t they?

How accurate is it? well, it definitely paints an extremely rosy picture for one specific case. However, I think it does highlight one very important point that is undeniably accurate, and that is using traditional methods to sell property on the open market can be a notoriously long process, which in itself comes at a cost that many don’t consider, and I think that’s what the comparison table shows above anything else. Time is money [and cash buying companies can save sellers a hell of a lot of time] .

Alternatives to Cash House Buying Companies

- Online Estate Agents: If you’re looking to sell cheaply, rather than necessarily quickly, you may want to consider using an online estate agent instead of a quick sale company. Online estate agents can market your property on major property portals such as Rightmove and Zoopla for as little as £99.

- High-Street Estate Agents: Before ruling out traditional high-street estate agents, it may be worth speaking with a few to see whether they can offer a “quick sale” strategy. It is also useful to ask about their average selling times. In many cases, a local estate agent may provide a more balanced approach between speed and sale price.

- Multi-Agent Strategy: If you’re open to using a high-street agent, it’s seriously worth considering a multi-agent approach, such as the service offered by flyp. This strategy involves multiple local estate agents marketing your property simultaneously, increasing exposure and potentially improving the chances of a quicker sale compared to a traditional sole-agency arrangement. They have received raving reviews, so it may be worth taking a look at flyp’s house selling service.

- Mortgage Lender Support Options: If your main reason for selling quickly is financial pressure, such as high mortgage repayments, it is worth contacting your mortgage lender to discuss your options. They may be able to offer payment adjustments or alternative arrangements to help you manage your situation.

Landlord out xo

Disclaimer: I'm just a landlord blogger; I'm 100% not qualified to give legal or financial advice. I'm a doofus. Any information I share is my unqualified opinion, and should never be construed as professional legal or financial advice. You should definitely get advice from a qualified professional for any legal or financial matters. For more information, please read my full disclaimer.

Guides")

Thanks for the great information.

I'm currently looking into using one of these companies to sell a few of my btl's. I was just wondering if you know why there is such a big difference in the percentage of the market value they offer? A spread between 75 - 90% can equate to alot of money. Do you have any thoughts? Many thanks